All Categories

Featured

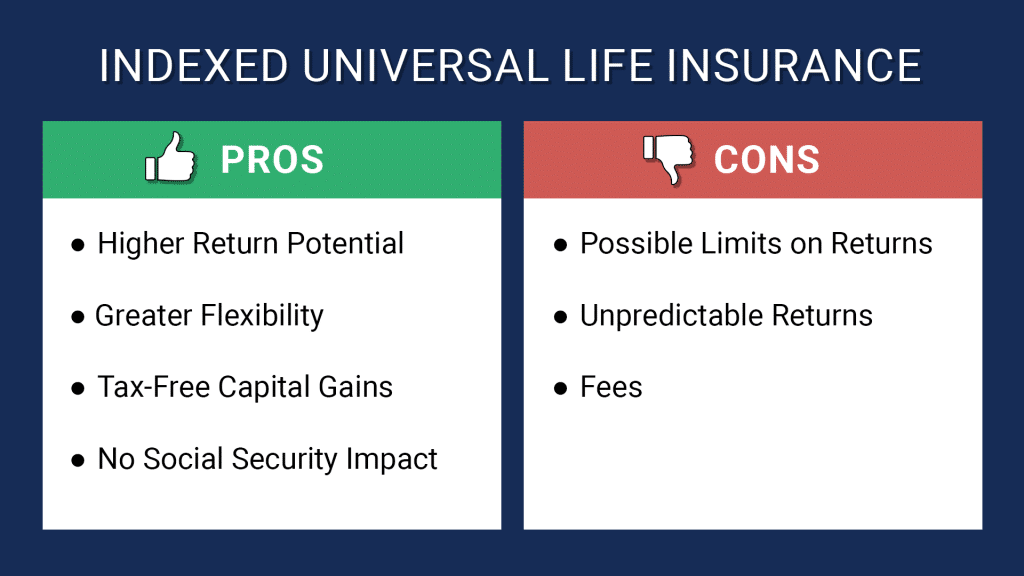

IUL agreements shield versus losses while offering some equity threat costs. High-net-worth individuals looking to minimize their tax worry for retirement might profit from spending in an IUL.Some financiers are better off acquiring term insurance coverage while maximizing their retired life strategy payments, instead than buying IULs.

If the underlying supply market index goes up in a provided year, owners will see their account boost by a symmetrical quantity. Life insurance policy business utilize a formula for establishing just how much to credit your cash balance. While that formula is linked to the efficiency of an index, the amount of the credit report is virtually always mosting likely to be much less.

With an indexed global life plan, there is a cap on the amount of gains, which can restrict your account's growth. If an index like the S&P 500 increases 12%, your gain can be a fraction of that amount.

Iul Life Insurance Dave Ramsey

Unalterable life insurance depends on have long been a prominent tax obligation shelter for such individuals. If you come under this group, think about talking with a fee-only monetary expert to review whether acquiring long-term insurance fits your overall approach. For several financiers, however, it may be far better to max out on payments to tax-advantaged pension, specifically if there are payment suits from a company.

Some plans have actually an assured price of return. One of the vital functions of indexed global life (IUL) is that it provides a tax-free circulations. So it can be a beneficial device for capitalists that want alternatives for a tax-free retired life. Typically, financial consultants would certainly advise contribu6ting to a 401(k) prior to an individual retirement account especially if your company is offering matching contributions.

Ideal for ages 35-55.: Deals versatile protection with modest money value in years 15-30. Some things customers should think about: In exchange for the fatality advantage, life insurance coverage items charge costs such as mortality and cost threat fees and abandonment fees.

Retired life preparation is critical to preserving economic safety and security and maintaining a details standard of living. of all Americans are bothered with "keeping a comfy requirement of living in retired life," according to a 2012 study by Americans for Secure Retired Life. Based on current statistics, this bulk of Americans are warranted in their concern.

Department of Labor approximates that a person will certainly need to keep their current requirement of living as soon as they start retired life. In addition, one-third of united state house owners, in between the ages of 30 and 59, will certainly not be able to maintain their criterion of living after retirement, even if they postpone their retirement until age 70, according to a 2012 study by the Employee Advantage Research Institute.

Www Walla Co Iul

In the exact same year those aged 75 and older held an ordinary financial obligation of $27,409. Amazingly, that number had even more than doubled since 2007 when the typical financial obligation was $13,665, according to the Employee Advantage Study Institute (EBRI).

56 percent of American senior citizens still had impressive financial obligations when they retired in 2012, according to a survey by CESI Financial debt Solutions. The Roth Individual Retirement Account and Policy are both devices that can be utilized to build substantial retirement savings.

These economic devices are similar in that they profit insurance holders that wish to produce savings at a reduced tax obligation price than they might run into in the future. However, make each more appealing for individuals with varying requirements. Establishing which is much better for you depends on your personal circumstance. The plan expands based on the rate of interest, or rewards, credited to the account.

That makes Roth IRAs suitable savings automobiles for young, lower-income workers who reside in a reduced tax bracket and who will certainly take advantage of decades of tax-free, compounded development. Considering that there are no minimum needed contributions, a Roth IRA gives financiers regulate over their individual objectives and run the risk of tolerance. Furthermore, there are no minimum called for circulations at any age during the life of the policy.

To compare ULI and 401K plans, take a minute to understand the essentials of both products: A 401(k) lets workers make tax-deductible contributions and take pleasure in tax-deferred development. When staff members retire, they usually pay taxes on withdrawals as regular revenue.

Transamerica Iul

Like various other permanent life policies, a ULI plan also assigns component of the premiums to a cash account. Considering that these are fixed-index policies, unlike variable life, the plan will certainly also have an ensured minimum, so the money in the money account will certainly not reduce if the index decreases.

Plan proprietors will additionally tax-deferred gains within their cash account. minnesota life eclipse iul. Check out some highlights of the benefits that global life insurance policy can supply: Universal life insurance policy policies don't impose limits on the dimension of plans, so they might supply a means for workers to conserve more if they have currently maxed out the Internal revenue service limitations for various other tax-advantaged economic products.

The IUL is much better than a 401(k) or an Individual retirement account when it comes to conserving for retirement. With his nearly 50 years of experience as an economic strategist and retirement preparation expert, Doug Andrew can show you exactly why this is the case.

%20Plans){kind=link}

Latest Posts

What's The Difference Between Whole Life And Universal Life Insurance

Adjustable Life Insurance Policies

Is Universal Life Whole Life